Covid-19 is the illness caused by the corona virus. This illness caused the death of millions around the world. According to World Health Organisation WHO Coronavirus (COVID-19) Dashboard, as of April 2021, there have been globally 133,552,774 confirmed cases of COVID-19, including 2,894,295 deaths. As of April 2021, a total of 669,248,795 vaccine doses have been administered.

Hope for the end of the pandemic started to loom in the horizon with the discovery of vaccines with long term efficiency yet to be proved.

This article sheds light on latest developments in COVID-19 vaccines technologies. These developments are put together and consolidated in a vaccine technology framework proposed by the Union of Arab Banks. This framework embraces COVID-19 vaccines knowledge repository, tracking dashboard, technologies, policy and guidance, production, operation, and impact on GDP, stock market, and various economic sectors. We conclude with recommendations to empower the vaccine technology framework in a global digital economy and GROW, BUILD, and DEPLOY the supporting global digital economy platform.

VACCINES BASICS

The World Health Organization WHO informs that vaccination is a simple, safe, and effective way of protecting people against harmful diseases. It helps the body to build resistance to specific infections and strengthen immunity. Vaccines train the immune system to create antibodies when exposed to a disease. Most vaccines are given by an injection, but some are given orally or sprayed into the nose.

COVID-19 VACCINES DASHBOARD

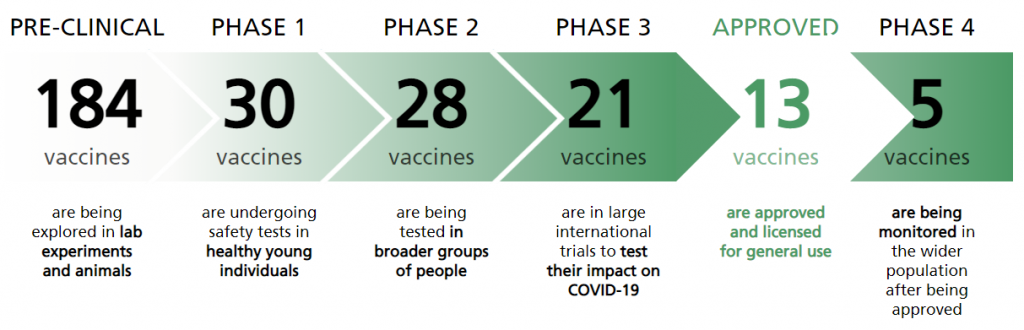

Gavi, The World Vaccine Alliance, tracked COVID-19 vaccines developed so far. According to Gavi sources, as of January 2021, two hundreds novel coronavirus vaccine candidates are under development, of which 64 are in clinical trials.

Figure 1: The COVID-19 VACCINE RACE (sources: Gavi, The World Vaccine Alliance)

The most widely used vaccines are developed by the following firms:

Pfizer and its German-based partner BioNTech

Moderna

Johnson & Johnson’s and Janssen Pharmaceuticals

AstraZeneca made with a team at Britain’s University of Oxford

Novavax: Maryland-based biotechnology company

Sanofi and GlaxoSmithKline

Sinovac and Sinopharm Chinese company

Sputnik V developed by Russian researchers

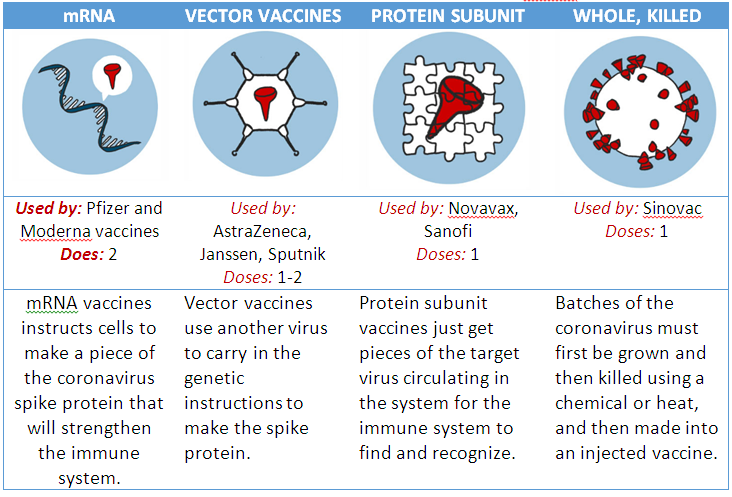

COVID-19 VACCINES TECHNOLOGIES

Various technologies were used in covid-19 vaccines innovated to date. These technologies are described in the following table.

Table 1. COVID-19 Vaccines technologies (Table adapted from Source: CNN Reporting; Graphic: Will Mullery, CNN)

MIT technology review, compiled an annual selection of the year 2021 most important technologies changing our lives. COVID-19 vaccine technology, mRNA was on the top of the list of these most important technologies.

VACCINE PRODUCTION

The World Health Organization WHO, The Centre for disease control and prevention CDC, UNICEF, and various healthcare authorities around the world are developing blueprints for various vaccines. These blueprints give the following information about vaccines and can be accessed online:

Overview of vaccine producer and development

Number of vaccines produced so far and supplied to the world

Doses required at various time intervals

How it is taken (oral, or injection, or other)

Storage requirement

Approval by authorities and countries around the world

Trial stage

Side effects

Long term impact

Repeating frequency (how often we need to retake the jab to stay immune)

Uptake and acceptance by various communities

Underlying technology

Contributing manufacturers and labs

Other info

There has been huge efforts from world organization and authorities to encourage people to take vaccine but some people around the world still have fears and concerns about vaccines side effect, impact on the body, short term and long term efficiency, and other concerns in respects of use, production, and appropriate supply.

VACCINE SUPPLY

KPMG analysis reveals that the emergence of COVID-19 vaccines has generated immense excitement, but healthcare systems around the world now face the complex task of securing and distributing supplies and administrating vaccines. Acquiring sufficient quantities is just the start. The vaccines must then be transported safely to multiple destinations, maintained at the right temperature, and tracked at all times to avoid tampering and assure product integrity and delivery.

The World Economic Forum foresees that vaccines to be effective in containing the pandemic, they must be made widely available across the globe in a short space of time, which is putting increased pressure on governments, multilateral organizations, manufacturers, supply chain companies and community organizations.

According to ESRI, the producer of the world’s most powerful mapping & spatial analytics software, and the International Air Transport Association, approximately 25 percent of shipped vaccines are compromised due to poor temperature management.

VACCINE GUIDELINES

The World Health Organisation WHO and UNICEF put the COVID-19 vaccination supply and logistics guidance in February 2021. The guidance provides details about vaccines profiles, supply strategies, COVAX Supply Chain , preplanning, core functions and logistics, deployment, operations, reception of vaccines, storage of vaccines, repackaging vaccines, production or purchase of coolant packs, transportation of vaccine, reverse logistics, managing recalls, management of supply chain information, traceability and vaccines rapid information, securing the supply chain, budgeting and financial management, vaccine store infrastructure and power requirements, health care waste management, human resources training, capacity building, and assessed country preparedness activities.

The COVID-19 Tools Accelerator COVAX facility is co-led by CEPI, Gavi and WHO, alongside key delivery partner UNICEF, and PAHO Revolving Fund America procurement agent for COVAX. COVAX aims to accelerate equitable access to appropriate, safe and efficient vaccines for all countries.

VACCINE POLICIES

According to CNN news, Microsoft, Oracle and other tech giants teamed up to develop Covid-19 vaccine passports. Biggest tech firms and health care organizations have joined together in the Vaccine Credential Initiative that ensures that everyone has access to a secure, digital record of their Covid-19 vaccination. This digital record is like a digital vaccine passport and can be used for everything from airline travel to entering concert venues. The coalition comprises a broad range of health care and tech leaders including Microsoft, Salesforce, Oracle, CERN, Cigna, Epic and the Mayo Clinic, and others.

IMPACT ON STOCK MARKET

According to the Guardian news, Pfizer chief sold $5.6m of shares on day of Covid-19 vaccine announcement.

CNBC news foresee that COVID-19 vaccines are creating market winners and losers and sparking optimism that the pandemic end may be approaching. Analysts see that vaccines are fuelling hope of a return to normal soon.

With wide vaccine rollout, it is expected that some sectors will benefit more than others. Possible winners include the aviation, the retail, the estate, followed by office and hospitality sectors.

IMPACT ON GDP

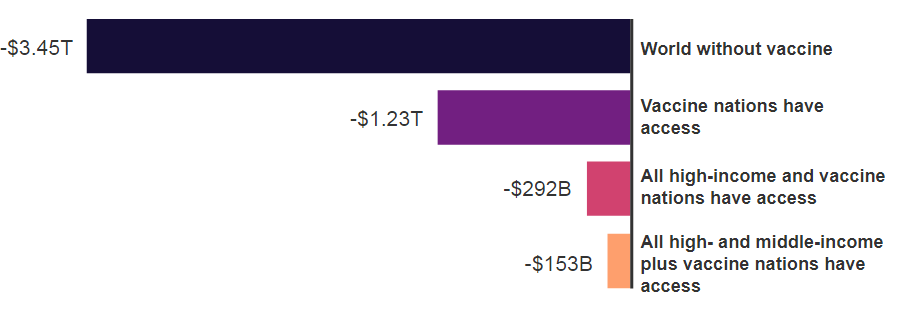

FOX news forecasts that coronavirus vaccine will drive to economic re-bounce and restore economic growth. Strategists expect 6% growth in global GDP.

RAND research estimated economic re-bounce and the impact of COVID-19 vaccines on global GDP change as follows:

In world without vaccine the expected Global GDP change is –$3.45 Trillions

In nations with vaccine access the expected Global GDP change is –$1.23 Trillions

In all high income nations with vaccine access the expected Global GDP change is –$292 Billions

In all high and middle income nations with vaccine access the expected Global GDP change is –$153 Billions

Figure 2. Impact of COVID-19 vaccines on Global GDP change (Sources: RAND research)

IMPACT ON DIGITAL DIVIDE

Covid-19 vaccine rollout revealed a digital divide problem around the world from unequal internet access. World organizations and authorities stressed the importance of digital literacy and closing the digital divide as everything from school to work shifted from physical to virtual interactions. Those without access to reliable internet or devices at home are not able to keep up with the pandemic challenges.

THE WAY FORWARD IN A GLOBAL DIGITAL ECONOMY

Large scale pandemics cannot be totally avoided but technologies of the digital economy can help in various respects:

Innovation in vaccine production;

Developing secure data infrastructure for digital vaccine passport;

Improving the global supply chain of vaccines world roll out;

Raising awareness and prevention;

Innovation in gadgets production

Bridging the digital divide

Adapting design to new life style like work from home

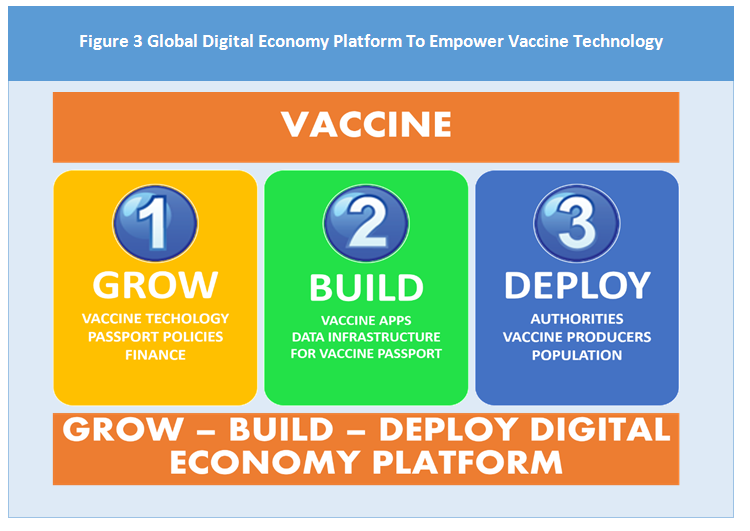

The suggested way forward for a strong immune digital economy is to GROW – BUILD – DEPLOY a global digital economy platform empowering the vaccine technology framework, as detailed below:

GROW

Grow knowledge and expertise in digital technologies for vaccine production.

Grow policies for digital passports with vaccine data records.

Grow finances to support innovation.

BUILD

Build digital apps and gadgets for vaccine production and illness prevention.

Build secure and high quality global data infrastructure that can help in sharing and analysing vaccine data.

DEPLOY

Deploy apps developed for free use by healthcare authorities, producers and developers of vaccines, and the population at large. These apps include:

Vaccine global supply chain management apps

Vaccine planning apps

Dashboard apps to track infection and vaccine supply

The World Union of Arab Bankers (WUAB) organized on the 15th of April, 2021 the “First Banking Executive Online Conference 2021” via visual communication technology.

The Conference which serves as a platform of communication among active people in the field, was attended by more than 120 participants from Arab Banks, financial institutions, Arab banking and financial organizations, unions and NGOs, as well as diplomatic, governmental and political personnel.

Among the prominent participants were Dr. Joseph Torbey, Chairman, World Union of Arab Bankers, and Chairman of the Executive Committee, Union of Arab Banks, Mr. Adnan Ahmed Yousif, Chairman of Bahrain Association of Banks, Mr. Mohamed El-Etreby, Federation of Egyptian Banks (FEB), H.E. Mr. Marwan Hamadeh, H.E Ms. Kholoud M. Saqqaf, CEO, Social Security Investment Fund –Jordan, H.E. Dr. Imad Boukhamseen, Board Member at the Union of Arab Banks (UAB), H.E. Dr. Mohammed Ben Omar, Secretary-General of the Arab organization of Information and Communication Technologies (ICT)

Conference Overview

I. The State of the World Economy

A stronger starting point for the 2021–22 forecast.

Multiple vaccine approvals and the launch of vaccination in some countries in December have raised hopes of an eventual end to the pandemic.

Three questions. These developments raise three interrelated questions for the global outlook.

How will restrictions needed to curb transmission affect activity in the near term before vaccines begin delivering effective society-wide protection?

How will vaccine-rollout expectations and policy support affect activity?

How will financial conditions and commodity prices evolve?

Fiscal policy support set to boost economic activity.

Supportive financial conditions. Major central banks are assumed to maintain their current policy rate settings throughout the forecast horizon to the end of 2022.

Rising commodity prices.

Risks of the Outlook

Although new restrictions following the surge in infections suggest growth could be weaker than projected in early 2021, other factors pull the distribution of risks in the opposite direction.

On the upside, further favourable news on vaccine manufacture (including on those under development in emerging market economies), distribution, and effectiveness of therapies could increase expectations of a faster end to the pandemic than assumed in the baseline, boosting confidence among firms and households.

On the downside, growth could turn out weaker than in the baseline if the virus surge (including from new variants) proves difficult to contain, infections and deaths mount rapidly before vaccines are widely available, and voluntary distancing or lockdowns prove stronger than anticipated. Slower-than-anticipated progress on medical interventions could dampen hopes of a relatively quick exit from the pandemic and weaken confidence.

II. Digital Transformation

Digital transformation is the integration of digital technology into all areas of a business, fundamentally changing how we operate and deliver value to customers. It’s also a cultural change that requires organizations to continually challenge the status quo, experiment, and get comfortable with failure.

The four domains in Digital Transformation.

Technology From the Internet of Things, to blockchain, to data lakes, to artificial intelligence, the raw potential of emerging technologies is staggering. And while many of these are becoming easier to use, understanding how any particular technology contributes to transformational opportunity, adapting that technology to the specific needs of the business, and integrating it with existing systems is extremely complex.

Data The unfortunate reality is that at many companies today most data is not up to basic standards, and the rigors of transformation require much better data quality and analytics. Transformation almost certainly involves understanding new types of unstructured data (e.g., a driver-supplied picture of damage to a car), massive quantities of data external to your company, leveraging proprietary data, and integrating everything together, all while shedding enormous quantities of data that have never been (and never will be) used.

Process Transformation requires an end-to-end mindset, a rethinking of ways to meet customer needs, seamless connection of work activities, and the ability to manage across silos going forward.

Organizational Change Capability In this domain we include leadership, teamwork, courage, emotional intelligence, and other elements of change management.

Pulling It All Together So far, we’ve discussed the technology, data, process, and organizational change capability domains as if they existed in isolation, which of course they don’t. Rather, they are part of a larger whole. Technology is the engine of digital transformation, data is the fuel, process is the guidance system, and organizational change capability is the landing gear. You need them all, and they must function well together. Finally, work on technology, data, and process must proceed in an appropriate sequence. It is generally accepted that there is no sense automating a process that doesn’t work, so in many cases, process improvement or reengineering must come first.

Five Key Lessons:

Figure out your business strategy before you invest in anything. Leaders who aim to enhance organizational performance through the use of digital technologies often have a specific tool in mind. “Our organization needs a machine learning strategy,” perhaps. But digital transformation should be guided by the broader business strategy.

Leverage insiders. Organizations that seek transformations (digital and otherwise) frequently bring in an army of outside consultants who tend to apply one-size-fits-all solutions in the name of “best practices.” Rely instead on insiders — staff who have intimate knowledge about what works and what doesn’t in their daily operations.

Design customer experience from the outside in. If the goal of DT is to improve customer satisfaction and intimacy, then any effort must be preceded by a diagnostic phase with in-depth input from customers.

Recognize employees’ fear of being replaced. When employees perceive that digital transformation could threaten their jobs, they may consciously or unconsciously resist the changes. If the digital transformation then turns out to be ineffective, management will eventually abandon the effort and their jobs will be saved (or so the thinking goes). It is critical for leaders to recognize those fears and to emphasize that the digital transformation process is an opportunity for employees to upgrade their expertise to suit the marketplace of the future.

Bring Silicon Valley start-up culture inside. Silicon Valley start-ups are known for their agile decision making, rapid prototyping and flat structures. The process of digital transformation is inherently uncertain: changes need to be made provisionally and then adjusted; decisions need to be made quickly; and groups from all over the organization need to get involved.

III. Laws and Regulations

Regulation is rising on the risk radar

Regulating Financial Risks

Regulating Non-Financial Risks

AML Regulations

Financial Reporting

Laws and Regulations and the cost of Compliance

Laws and Regulations in the Digital Age

Laws and Regulations and the Competitive Environment

Laws and Regulations and the cost of operations.

Conference Proceedings

Inauguration

On Thursday April 15th, 2021 at 11:00 Beirut time, the “First Banking Executive Online Conference 2021” commenced by an introductory video about the World Union of Arab Banks.

Mr. Wissam H. Fattouh, Secretary General, Union of Arab Banks and World Union of Arab Banker welcomed the participants in his inauguration speech and explained the importance of the conference and the role it aims to play as a platform to share and exchange knowledge and discuss the latest developments the economy and banking sector is witnessing.

Dr. Joseph Torbey, Chairman, World Union of Arab Bankers, and Chairman of the Executive Committee, Union of Arab Banks, had a welcome speech, greeting the participants and highlighting the main effects and repercussions of Covid-19 pandemic on the global economy and the economies of the MENA region. Dr. Torbey then discussed the status of digital transformation and the huge leaps it has achieved especially during the pandemic and role it is playing in financial inclusion. However, Dr. Torbey emphasized that laws and regulation should develop rapidly to keep up the pace with the advancements in financial technology therefore creating opportunities to banks, supervisory bodies and clients as well.

Sessions

World Economy amidst the Pandemic

H.E. Mrs Kholoud El-Saqqaf, Chairman, Social Security Investment Fund – Jordan

Digital Transformation – Roadmap to Implementation

Dr. Leila Dagher, Associate Professor of Economics and the Director of the Institute of Financial Economics, American University of Beirut (AUB)

Dr. Mohammad Fheili, Risk Strategist and Capacity Building Expert

Modernization of Financial Laws and Regulations

Mr. Chahdan E. Jebeyli, Group Chief Legal & Compliance Officer, Bank Audi Group

Dr. Mohamad Hussein Mansour, Consultant at the World Bank Group, Director of the European Middle East Institute for Research, Lecturer at AUB and LAU

The 2021 Annual Meetings of the World Bank Group (WBG) and the International Monetary Fund (IMF) which took place virtually from Monday, April 5, through Sunday, April 11, 2021 brought together central bankers, ministers, parliamentarians, and other public sector representatives and officials along with private sector executives, and academics to discuss issues of global concern, including the world economic outlook, poverty eradication and economic development and most importantly the repercussions of the Covid-9 and recovery track.

This year the meetings featured seminars, regional briefings, press conferences, and many other events that focused on several global issues on economy, international development, and the world’s financial system. The meetings main focus was on a pandemic and post pandemic world, vaccination and road to recovery.

The event included meetings of the Development Committee, the International Monetary and Financial Committee (IMFC) and the Coalition of Finance Ministers for Climate Action. The participants identified challenges going forward, including: slowing global growth; insufficient investment rates in developing countries; climate change and extreme weather; fragility, conflict and violence, crisis management, gender inequality, knowledge, regional integration, energy security, biodiversity, illicit financial flows and pandemics.

INTERGOVERNMENTAL GROUP OF TWENTY-FOUR ON INTERNATIONAL MONETARY AFFAIRS AND DEVELOPMENT COMMUNIQUÉ

7 April 2021

Chaired by Abdolnaser Hemmati, Governor of the Central Bank of the Islamic Republic of Iran

The global economy is showing signs of recovering from the COVID-19 crisis. The path to broad-based and inclusive recovery is nevertheless fraught with uncertainty about the availability and access to safe and affordable vaccines for all and the strength of external financial support to developing countries. The pandemic has strained the health systems and severely hit the economies of developing countries, which have had limited policy space to respond. Millions of people have fallen into extreme poverty, and food insecurity has risen starkly especially in the poorest countries and those living in fragile and conflict-affected situations. Our urgent priorities are to contain the pandemic, for which scaling up vaccinations will be crucial, and rebuild our economies to avoid a lost decade of development and a major decline in people’s well-being.

At this critical juncture, international cooperation is essential to secure a better recovery for all countries and promote a strong pace of global convergence of per capita income levels between advanced and developing countries. We will continue to respond with exceptional policy measures, as long as needed and as national circumstances allow it, in order to support economic activity to protect jobs and incomes, provide social protection especially to vulnerable populations, strengthen health systems, accelerate digitalization and maintain financial resilience. Large stimulus packages in advanced countries cushioned the global impact of the pandemic, and we encourage them not to withdraw support prematurely. International assistance for developing countries, however, has fallen short of their estimated $2.5 trillion in additional financing needs. We call on the IFIs, especially the IMF and the World Bank, in coordination with the international community to ensure the availability, to the fullest extent possible, of the necessary liquidity and fiscal support for all developing countries. Concessional financing and ensuring positive net transfers should be essential parts of the global financial response to avoid prolonged damage to development prospects of low-income countries (LICs) and small vulnerable states. It is crucial for all major economies to work together and use all policy tools available to foster an environment of increased trade and investors’ confidence to boost investment growth for all countries.

Early availability of, and equitable access to, affordable vaccines everywhere is the most critical public good at this juncture. It is essential to contain the pandemic and secure a broad-based global recovery. We call on advanced countries to boost financing for the COVAX Facility to help more low- and middle-income countries obtain fair and rapid access to affordable vaccines and move toward patent liberalization for COVID-19 vaccines to boost global production. We welcome the African Union’s vaccine program that procures vaccines to supplement those acquired through the COVAX Facility. Multilateral development banks (MDBs) must also play an important role in financing and delivering vaccines and support efforts to enable vaccine manufacturing in developing countries. We call on MDBs to enhance international cooperation and uniformly adopt the COVAX vaccine criteria or the World Health Organization (WHO) Emergency Use List. At this time, developing countries’ access to vaccines is constrained by existing supply, which has mostly been purchased by advanced economies. We call on the World Trade Organization and MDBs to seek solutions to scale up the production of vaccines, including addressing intellectual property rules to expand the manufacturing of vaccines and other medical products to effectively deal with the COVID-19 pandemic.

We reiterate the importance of a strong global financial safety net, with an adequately resourced, quota-based IMF at its center. We welcome the stronger support in the IMF’s Executive Board for a meaningful new allocation of Special Drawing Rights (SDRs) to address long-term global liquidity needs. This must be made alongside commitments from members with strong external positions to voluntarily channel their SDRs, including from the new allocation, to benefit countries in need of liquidity support in these exceptional times. Recycling mechanisms that boost IMF’s lending capacity will enable the Fund to increase access limits for borrowers and provide additional support to low- and middle-income countries. Going forward, the IMF should take steps to modernize and enhance the impact of SDRs, including considering a more equitable and just way to allocate SDRs across countries to take account of demand. We urge the IMF to ensure utilization of SDRs in a transparent and accountable manner. We further urge the IMF to ensure the timely completion of the 16th General Review of Quotas by end-2023, and look forward to increased quota resources, reduced reliance on borrowed resources and the implementation of long-awaited governance reforms to increase the quota share of emerging markets and developing countries while protecting the shares of the poorest countries.

We commend the swift response of the IMF to support its member countries since the onset of the pandemic. Going forward, it is important for the IMF to flexibly adapt its lending toolkit to the evolving needs of low- and middle-income countries during their recovery. We draw attention to the role of precautionary financing instruments in helping eligible countries deal with tail external risks. Since this is the year for the IMF to review its Access Limits as well as its Surcharge Policy, we urge the Fund to correct the regressive and pro-cyclical character of the Surcharge Policy and consider specific measures, such as suspending surcharges at this time to help countries’ economic recovery. We encourage the IMF to further consider a significant permanent reduction in surcharges or their elimination. In addition to seeking new donor resources, we encourage the Fund to explore non-traditional and predictable funding options to boost the Poverty Reduction and Growth Trust’s resources as well as to increase the IMF’s own resources devoted to capacity development that has been increasingly sought by countries. We urge the IMF to find the means to increase its internal budget resources to ensure that it has the necessary financial and human resources to fulfill its mandate. We look forward to the upcoming review of the IMF’s Institutional View on Capital Flows which should aim to help countries reap the benefits of capital flows while managing risks to ensure stability.

It is crucial to support developing countries in managing their worsening debt vulnerabilities to avoid a debt crisis that retards development progress and enable countries to accelerate growth and regain debt sustainability. The G20’s Debt Service Suspension Initiative (DSSI) has provided short-term breathing space for many LICs, more than half of which are under high risk of debt distress or in distress. Debt treatments may be needed for some countries to put them on the path to achieve debt sustainability. In this regard, we welcome the G20’s Common Framework for Debt Treatments (CF) beyond the DSSI. We look forward to fair, meaningful and expeditious sovereign debt treatments, with participation of private creditors, within the CF. We encourage the IMF and the World Bank Group (WBG) to support the implementation of the CF in line with their mandates, provide exceptional financial support to strengthen the capacity of countries to undertake debt treatments when sought and enhance debt management frameworks, including transparency of debtor and creditor countries and reporting standards. Realistic debt sustainability assessments are necessary to determine the depth of the financing needed. We encourage MDBs to support low- and middle- income countries in need of debt relief, including through innovative instruments to reduce debt burdens and ensuring significant positive net transfers. The effective implementation of the CF in a way that moderates market and credit rating agency reactions could encourage eligible countries to seek timely debt treatment, when needed. We reiterate our call for increased multilateral efforts to improve the architecture for sovereign debt resolution to facilitate expeditious debt treatments.

Severe fiscal constraints and heightened debt vulnerabilities imperil our ability to contain the pandemic and invest to build back our economies in an inclusive, resilient and sustainable manner. The WBG and other MDBs should use the strength of their balance sheets to scale up financial support to both low- and middle-income countries. We commend the WBG’s frontloaded International Development Association (IDA) lending program. We look forward to the successful completion of IDA20 replenishment in end-2021. The WBG should strengthen its financial support for middle-income countries and consider waiving front-end and commitment fees to help countries recover. We urge the WBG to explore options to stretch its balance sheets to the fullest extent possible to boost their medium-term lending capacity, including greater flexibility in implementing individual country lending limits. Shareholders should monitor and address constraints to MDBs’ lending capacity in a timely way.

Developing countries will need to explore all sources of financing to rebuild fiscal buffers as their economies recover and ensure effective use of resources. Countries should explore avenues to ensure that taxes can contribute to raise revenues, address inequality, improve health outcomes and promote a sustainable recovery. We urge the IMF and the WBG to further strengthen support for capacity building for domestic resource mobilization and public debt and expenditure management. We call on the IMF and the WBG to enhance their support to address the challenges faced by small states, fragile and conflict-affected states and countries hosting refugees and experiencing significant migration influx. We urge the WBG and other MDBs to explore innovative and effective solutions, including de-risking instruments, to leverage more private financing in sustainable energy and other infrastructure investments as well as initiatives to support small and medium enterprises.

We call for multilateral cooperation to reform international tax rules and practices to prevent further erosion of our tax bases. On the taxation of the digital economy, we look forward to a fair and equitable multilateral solution that addresses concerns of developing countries and the taxation challenges of digitalization. We seek a solution that yields meaningful and sustainable revenues for developing countries by enabling them to tax their fair share of the profits of multinationals in this digital age. The solution should be simple to implement and comply with. Additionally, we urge the IMF and the WBG to deepen their work to measure, monitor, and contain illicit financial flows.

We welcome the stronger international support for an inclusive and sustainable recovery. Delivering on climate finance by the global community is a critical and fair way to assist developing countries to implement their Nationally Determined Contributions to meet climate goals. Advanced countries should fulfill their commitment, under the 2009 Climate Accord, to provide $100 billion annually by 2020 at the earliest possible time. It is critical to scale up currently meager amounts of concessional resources and finance for adaptation. Adequate financing and technical assistance from MDBs and climate-related funds will be crucial to support sustainable investments, especially infrastructure and energy, and leverage more private financing.

The Bretton Woods Institutions play important roles in assisting developing countries rebuild better and contribute to global climate goals. As they strengthen climate actions in programs, we ask that they tailor their assistance to the diverse circumstances of developing countries. We ask the WBG and other MDBs to support borrower countries pursue paths to a more sustainable recovery that consider countries’ current economic structures. These should result in a balanced integration of climate objectives with the achievement of the sustainable development goals. In this regard, MDBs should also strengthen their work on approaches to increase productivity, diversify economies and foster job-creating inclusive growth. We urge the MDBs and the IMF to articulate better the elements of their assistance strategies, within their comparative advantages and in line with their mandates, to support developing countries of diverse circumstances transition to more inclusive and sustainable economies.

Second G20 Finance Ministers and Central Bank Governors Meeting Communique – Italian G20 Presidency

7 April 2021

After the sharp contraction in 2020, the global outlook has improved mainly due to the roll out of vaccination campaigns and continued policy support. However, the recovery appears uneven across and within countries, fragile and subject to elevated downside risks, including the spread of new variants of the COVID-19 virus and different paces of vaccination. We will address the problem of economic scarring, especially on those most impacted, including women, youth, informal and low-skilled workers. We commit to remaining vigilant and avoiding any premature withdrawal of support measures. We reaffirm our resolve to use all available policy tools for as long as required to protect people’s lives, jobs and incomes, to support the global economic recovery, fight rising inequalities, and enhance the resilience of the financial system, while safeguarding against downside risks and negative spillovers and preserving long-term fiscal sustainability.

Overcoming the pandemic is a precondition for a stable and lasting recovery. We remain committed to strengthening health systems and facilitating equitable and swift access to safe, effective and affordable COVID-19 vaccines, therapeutics and diagnostics and we encourage efforts to rapidly step up their production and distribution. In this regard, we recognize the role of COVID-19 immunization as a global public good and reiterate our support to all collaborative efforts, especially to the four pillars of the Access to COVID-19 Tools Accelerator (ACT-A) and its COVAX Facility. We emphasize the need to enhance cooperation and policy coherence with and among multilateral organizations, especially with the World Health Organization. We look forward to the recommendations of the G20 High Level Independent Panel on Financing the Global Commons for Pandemic Preparedness and Response in July.

Strong fundamentals and sound policies are essential to the stability of the international monetary system. We remain committed that our exchange rates reflect underlying economic fundamentals and note that exchange rate flexibility can facilitate the adjustment of our economies. We will continue to consult closely on foreign exchange market developments. We recognize that excessive volatility or disorderly movements in exchange rates can have adverse implications for economic and financial stability. We will refrain from competitive devaluations and will not target our exchange rates for competitive purposes.

We acknowledge the important role of open and fair rules-based trade in restoring growth and job-creation. We recall our commitment to fight protectionism and we encourage concerted efforts to reform the World Trade Organization.

The G20 Action Plan, endorsed on 15 April 2020 and updated last October, sets out the key principles guiding our response, taking into account country-specific conditions. We welcome the Third Progress Report (Annex 1), which takes stock of the significant progress made against our commitments so far. Recent health and economic developments and persisting downside risks call for strong policy actions, enhanced multilateral coordination and continued support to the most vulnerable. We therefore endorse the second update of the G20 Action Plan (Annex 2) setting a forward-looking agenda to tackle current and future global challenges. In line with the Riyadh Leaders’ Declaration of November 2020, we reiterate our commitment to keeping the G20 Action Plan a living document and to regularly review, update, track implementation of, and report on it.

We concur on the need to harness the opportunities stemming from technological innovation to boost the recovery and ensure broad-based prosperity. We look forward to the G20 Menu of Policy Options on productivity-enhancing digital transformation, which will provide good practices for harnessing the opportunities offered by digitalization while ensuring that these opportunities are shared within and across countries. We welcome ongoing efforts for strengthening global risk monitoring and look forward to integrating it more systematically into future policy discussions where appropriate. We will continue to closely coordinate our efforts to enhance resilience against future shocks, including pandemics, natural disasters, climate and environmental risks. We also recognize that improving data availability and provision, including on environmental issues, and harnessing the wealth of data produced by digitalization, while ensuring compliance with legal frameworks on data protection and privacy, will be critical to better inform our decisions. We therefore ask the International Monetary Fund (IMF), in close cooperation with the Inter-Agency Group on Economic and Financial Statistics (IAG) and the Financial Stability Board (FSB), to prepare a concept note on a possible new Data Gaps Initiative.

Tackling climate change and promoting environmental protection are increasingly urgent for our economies and societies. Shaping the recovery provides a unique opportunity to develop forward-looking strategies investing in innovative technologies and promoting just transitions toward more sustainable economies and societies, with particular attention to the most affected segments of the population and in line with the Paris Agreement. We look forward to discussing how to better coordinate and deliver such strategies to achieve our shared agenda. We encourage international organizations to monitor recovery strategies and provide further analysis on the impact of climate change and de-carbonization measures on growth and employment, in line with their respective mandates.

We acknowledge that mobilizing sustainable finance is essential for global growth and stability and for promoting the transitions towards greener, more resilient and inclusive societies and economies. We ask the FSB to work on evaluating the availability of data and data gaps on climate-related financial stability risks, and on ways to improve climate-related financial disclosures, and to report on these subjects in July. We agree on the importance of promoting globally consistent, comparable high-quality standards of disclosure for sustainability reporting, building on the recommendations of the FSB’s Task Force on Climate-related Financial Disclosures. We welcome growing private sector participation. We also take note of growing public sector participation and transparency in these areas. We welcome the re-establishment of the Sustainable Finance Study Group, which we are upgrading to a working group, and we look forward to its work, for 2021, on developing, in a collaborative manner, an initial evidence-based and climate-focused G20 sustainable finance roadmap, improving sustainability reporting, identifying sustainable investments, and aligning International Financial Institutions’ efforts with the Paris Agreement. We also look forward to continuing the discussion on these issues at the Venice Conference on Climate, which will be held on 11 July.

We recognize the critical role of quality infrastructure investments in the recovery phase. Promoting resilient, sustainable and inclusive infrastructure will be key to stimulating economic growth and development. We welcome the creation of the InfraTracker by the Global Infrastructure Hub (GIH), which can help to better inform our policy decisions and shape our stimulus packages. We will explore infrastructure potential in creating jobs for supporting a robust and sustainable recovery. We take note of the IMF Note on Environmentally Sustainable Investment for the Recovery. In line with the G20 Roadmap to Infrastructure as an Asset Class and building on the G20/OECD Report on the Collaboration with Institutional Investors and Asset Managers on Infrastructure, we will continue, in a flexible manner, the dialogue between public and private investors to mobilize private capital. We will continue to explore innovative financial instruments to bridge the infrastructure financing gap. We agree to develop a G20 Policy Agenda on infrastructure resilience and maintenance. We will work to improve financing of digital infrastructure and extend coverage of underserved areas, including through fostering investments for high-quality broadband connectivity. We will encourage knowledge sharing with the representatives from local authorities to facilitate enhanced coordination with national governments to achieve more inclusive societies. We welcome advancing the work related to the G20 Principles for Quality Infrastructure Investment (QII). In this regard, we welcome the GIH QII Survey Report. We recall our previous agreement on exploring possible indicators on QII and look forward to the outcome of the Infrastructure Working Group work in this area. We reiterate the need to better inform infrastructure investment decisions, including through the ongoing work of related initiatives by international organizations on access to data, such as the Infrastructure Data Initiative.

We will further step up our support to vulnerable countries as they address the challenges associated with the COVID-19 pandemic. We call on the IMF to make a comprehensive proposal for a new Special Drawing Rights (SDR) general allocation of USD 650 billion to meet the long-term global need to supplement reserve assets. A new allocation would enhance global liquidity and will help the global recovery, building on the last assessment made by the IMF in 2016. We also invite the IMF to present proposals to enhance transparency and accountability in the use of the SDRs while preserving the reserve asset characteristic of the SDRs. In parallel, we ask the IMF to explore options for members to channel SDRs on a voluntary basis to the benefit of vulnerable countries, without delaying the process for a new allocation.

We welcome the progress achieved by the Debt Service Suspension Initiative (DSSI) in facilitating higher pandemic-related spending. All official bilateral creditors should implement this initiative fully and in a transparent manner. In light of the persistence of significant liquidity needs related to COVID-19, we agreed to its final extension by 6 months through end-December 2021, which is also agreed by the Paris Club. We reiterate our call on the private sector, when requested by eligible countries, to take part in the DSSI on comparable terms. This final extension will allow beneficiary countries to mobilize more resources to face the challenges of the crisis and, where appropriate, to move to a more structural approach to address debt vulnerabilities including through an Upper Credit Tranche quality IMF-supported program. Within this context, we welcome the ongoing efforts to implement the Common Framework for Debt Treatments beyond the DSSI to address debt vulnerabilities on a case-by-case basis and look forward to the coming first meeting of the first creditor committee. In each case, we are committed to implementing the Common Framework in a coordinated manner, including through sharing necessary information among participating official bilateral creditors. The joint creditors’ negotiation shall be held in an open and transparent manner and before finalization of the key parameters, due consideration shall be given to the specific concerns, if any, of all participant creditors and the debtor country. In this regard, we note that the need for debt treatment, and the restructuring envelope that is required, will be based on an IMF/World Bank Group (WBG) Debt Sustainability Analysis and the participating official creditors’ collective assessment. We ask the IMF/World Bank (WB) to support the implementation of the Common Framework, in line with their respective mandates. We stress the importance for private creditors and other official bilateral creditors of providing debt treatments under the Common Framework on terms at least as favorable, in line with the comparability of treatment principle. We reiterate the importance of joint efforts by all actors, including private creditors, to continue working towards enhancing debt transparency. We recall the forthcoming work of the Multilateral Development Banks (MDBs), as stated in the Common Framework, in light of debt vulnerabilities. We look forward to progress by the IMF and WBG on their proposal of a process to strengthen the quality and consistency of debt data and improve debt disclosure. We welcome the launch of a second voluntary self-assessment of the implementation of the G20 Operational Guidelines for Sustainable Financing. We look forward to further updates on the implementation of the Institute of International Finance Voluntary Principles for Debt Transparency.

We welcome MDBs commitments of USD 75 billion to DSSI-eligible countries over the period between April 2020 – December 2020, as part of their USD 230 billion commitment to support emerging and low-income countries in response to the COVID-19 pandemic. We also welcome USD 12.4 billion in financing provided to low-income countries by the IMF since the start of the pandemic and mobilization of about USD 24 billion in new loan resources for the Poverty Reduction and Growth Trust (PRGT). We welcome the contributions provided to date to the Catastrophe Containment and Relief Trust (CCRT) and call on more contributions so that debt service relief can be provided until April 2022.

Going forward, the IMF estimates that low-income countries would need to deploy around USD 200 billion up to 2025 to step up response to the pandemic and build external buffers and an additional USD 250 billion in investment spending to accelerate their income convergence with advanced economies. We will deploy all tools to help countries close this financing gap. In recognition of the critical role of the International Development Association (IDA), we welcome advancing IDA-20 by one year. An ambitious and successful IDA replenishment by December 2021, underpinned by a strong policy framework, will support a green, resilient and inclusive recovery in IDA countries as they address both the immediate and longer-term impacts of the pandemic. We call on IDA to explore how to further use its own balance sheet to unlock additional resources for IDA countries in a sustainable manner while maintaining its AAA rating. We call on the WBG to scale up its efforts to mobilize private financing. We also call on the IMF to enhance its concessional lending capacity and to explore, together with its members, additional options to mobilize resources to support vulnerable countries, including through the PRGT and the CCRT. We also call on the IMF to explore additional tools for all vulnerable countries. We encourage MDBs to make the best use of available resources to serve their clients, including by implementing the G20 Action Plan on Balance Sheet Optimisation. We also encourage further progress on exploring potential new measures to maximize their development impact, according to their respective mandates and while protecting their credit ratings. We reaffirm the importance of enhancing coordination among development partners at multilateral, regional and country level. We look forward to further updates by MDBs on progress in implementing country-owned pilot platforms.

We reiterate our commitment to strengthening long-term financial resilience and supporting inclusive growth, including through promoting sustainable capital flows, developing local currency capital markets and maintaining a strong and effective Global Financial Safety Net with a strong, quota-based, and adequately resourced IMF at its center. We look forward to the forthcoming review of the IMF’s Institutional View on the liberalization and management of capital flows. We welcome the preservation of the overall IMF lending capacity recently accomplished through the doubling of the New Arrangements to Borrow and a new round of Bilateral Borrowing Agreements. We remain committed to revisiting the adequacy of IMF quotas and will continue the process of IMF governance reform under the 16th General Review of Quotas, including a new quota formula as a guide, by December 15, 2023.

We will continue our cooperation for a globally fair, sustainable, and modern international tax system. We remain committed to reaching a global and consensus-based solution building on the solid basis of the Reports on the Blueprints for Pillar 1 and Pillar 2, by mid-2021. We acknowledge the progress made to date and urge the G20/OECD Inclusive Framework on Base Erosion and Profit Shifting (BEPS) to address the remaining outstanding issues with a view to achieving an agreement by the set deadline. We acknowledge the progress made on implementing the internationally agreed tax transparency standards and support the Organization for Economic Cooperation and Development’s (OECD) ongoing work to explore proposals for automatic exchange of information on crypto-assets. We look forward to a constructive discussion at the High Level Tax Symposium on Tax Policy and Climate Change in July. We take note of the OECD updated report on Tax and Fiscal Policy in Response to the COVID-19 Crisis. We reaffirm our engagement to support developing countries in strengthening the capacity to build sustainable tax revenue bases and ask the OECD to prepare a report on progress made through their participation at the G20/OECD Inclusive Framework on BEPS and identify possible areas where domestic resource mobilization efforts could be further supported.

We commit to maintaining a comprehensive and united effort to respond to the COVID-19 crisis and ensuring that the financial sector continues to provide support to the economy, while preserving financial stability. We reiterate our commitment to the FSB’s principles agreed in April 2020 underpinning the national and international responses to COVID-19. Most of the support measures will remain in place for as long as economic and health circumstances require, recognizing that there are potential risks arising from withdrawing them too early. We welcome the FSB report discussing the benefits of a flexible state-contingent approach when considering whether to extend, amend, or end support measures, in a gradual and targeted way, to minimize long-term financial stability risks. We call on the FSB to continue to support international coordination on COVID-19 response measures in relation to financial stability, including through information sharing and through monitoring consistency with the agreed international standards.

We welcome the FSB evaluation report on the effectiveness of too-big-to-fail (TBTF) reforms for systemically important banks. We take note of the key findings that effective TBTF reforms bring net benefits to the society and we will work to address the gaps in reforms identified in the evaluation. We commit to taking stock of the lessons learned from the pandemic from a financial stability perspective. Building upon the FSB “Holistic Review” of the March 2020 market turmoil, we will work to strengthen the resilience of the non-bank financial intermediation (NBFI) sector with a systemic perspective and look forward to the FSB presenting a consultation report on policy proposals to enhance money market fund resilience in July, a final report in October and an update on the broader workplan for NBFIs. We commit to a timely and effective implementation of the G20 Roadmap to enhance cross-border payments, endorsed at the G20 Riyadh 2020 Summit, also to facilitate the flow of remittances. We look forward to the FSB progress report on how regulatory, supervisory and oversight frameworks address so-called “global stablecoins”, and to a broad discussion on the cross-border use of central bank digital currencies and wider implications for the international monetary system. We reiterate that no so-called “global stablecoins” should commence operation until all relevant legal, regulatory and oversight requirements are adequately addressed through appropriate design and by adhering to applicable standards. We look forward to the FSB report on harmonization of cyber incident reporting in the financial sector. We also look forward to a progress report on transition away from LIBOR. We welcome the additional clarity provided by the announcements of cessation dates for LIBOR benchmarks and reiterate the importance of orderly transition before end-2021.

We reaffirm our support for the Financial Action Task Force (FATF), as the global standard-setting body for preventing and combating money laundering (ML), terrorist financing (TF) and proliferation financing (PF). We look forward to the outcomes of the FATF’s current works on opportunities and challenges of digital transformation in tackling financial crime. We acknowledge the relevance of the second 12-month review on the global implementation of the FATF standards on virtual assets and virtual assets service providers, recognising that so-called stable coins are covered by the FATF standards. We welcome ongoing work especially by the FATF on the links between environmental protection and the prevention of corruption and illicit finance associated with the illegal exploitation of natural resources, recognizing the impact of environmental crime on climate and bio-diversity. We confirm our commitment to tackling all sources, techniques and channels of ML/TF/PF, deserving a particular attention to COVID-19-connected financial crimes. We commit to further strengthening the FATF’s Global Network of regional bodies in order to reinforce the effective implementation of the FATF standards.

Building on the G20 Financial Inclusion Action Plan endorsed last year, we support the Global Partnership for Financial Inclusion’s (GPFI) efforts to identify and address the gaps in financial inclusion that may have widened during the COVID-19 crisis, especially for the most vulnerable and underserved, as well as for micro, small and medium-sized enterprises. We also welcome the GPFI continued focus on remittances, including on reducing their transfer costs. We encourage the formulation of a menu of policy options informed by qualitatively robust, and to the fullest extent possible, granular data to help guide the appropriate response, depending on specific country needs, capabilities, and circumstances, including in the areas of digital financial literacy, consumer protection and financial business conduct, leveraging the opportunities offered by responsible digital financial services in enhancing financial inclusion, while safeguarding from risks.

World Bank/IMF Spring Meetings 2021: Development Committee Communiqué

The Development Committee met virtually today, April 9, 2021.

The COVID-19 pandemic has caused an unprecedented public health, economic, and social crisis, threatening the lives and livelihoods of millions. The economic shock is increasing poverty, worsening inequalities, and reversing development gains. As the global economy begins a gradual recovery, uncertainty surrounds near- and medium-term prospects. We call for sustained, differentiated, and targeted financial and technical support for an adequate policy response, strong coordination across bilateral and multilateral organizations, and further support to the private sector. We urge the World Bank Group (WBG) and the International Monetary Fund (IMF), in line with their respective mandates, to work closely together and with other partners to contain the impacts of the pandemic. We also ask the WBG to continue its support to countries in achieving the twin goals of ending extreme poverty and boosting shared prosperity and to promote green, resilient, and inclusive development (GRID), as well as support for the SDGs.

Timely delivery of safe and effective vaccines across all countries is critical to ending the pandemic, especially as new variants emerge. Developing countries need to strengthen their readiness for vaccination campaigns and develop coordinated strategies to reach vulnerable populations. We commend the WBG for supporting client countries’ procurement and deployment of vaccines, and we encourage strong monitoring and accountability mechanisms to ensure fair and efficient distribution. We welcome the WBG’s partnerships with WHO, COVAX, GAVI, UNICEF, and others, including private manufacturers, to help ensure that developing countries have fast, transparent, affordable, and equitable access to vaccines. We welcome WBG’s ongoing revision of the eligibility criteria for vaccine procurement. We call on IFC to redouble its efforts to support manufacturing capacity for vaccines and pandemic related medical supplies in developing countries. The pandemic has triggered far-reaching consequences, and we must strengthen global preparedness for future pandemics, and at the same time make progress in building robust health systems with universal coverage.

As poorer countries face the crisis with increased resource constraints, limited fiscal space, and rising public debt levels, more of them, including small states, are vulnerable to financial stress. The rapid initial response under the Debt Service Suspension Initiative (DSSI) has provided much- needed liquidity for IDA countries. We welcome the progress achieved by the DSSI in facilitating higher pandemic-related spending. All official bilateral creditors should implement this initiative fully and in a transparent manner. In line with the G20 decision, we support a final extension of the DSSI by 6 months through end December 2021, which is also agreed by the Paris Club. We reiterate our call on the private sector, when requested by eligible countries, to take part in the DSSI on comparable terms. This final extension will allow beneficiary countries to mobilize more resources to face the challenges of the crisis and, where appropriate, to move to a more structural approach to address debt vulnerabilities including through an Upper Credit Tranche quality IMF-supported program. Within this context, we welcome the ongoing efforts to implement the Common Framework for Debt Treatments beyond the DSSI to address debt vulnerabilities on a case-by case basis and look forward to the coming first meeting of the first creditor committee. In each case, we also welcome implementing the Common Framework in a coordinated manner, including through sharing necessary information among participating official bilateral creditors. The joint creditors’ negotiation shall be held in an open and transparent manner and before finalization of the key parameters, due consideration shall be given to the specific concerns, if any, of all participant creditors and the debtor country. In this regard, we note that the need for debt treatment, and the restructuring envelope that is required, will be based on an IMF/Bank Debt Sustainability Analysis and the participating official creditors’ collective assessment. We ask the World Bank and the IMF to support the implementation of the Common Framework, in line with their respective mandates. We stress the importance for private creditors and other official bilateral creditors of providing debt treatments under the Common Framework on terms at least as favorable, in line with the comparability of treatment principle. We recall the forthcoming work of the Multilateral Development Banks (MDBs), as stated in the Common Framework, in light of debt vulnerabilities. We look forward to progress by the IMF and WBG on their proposal of a process to strengthen the quality and consistency of debt data and improve debt disclosure. We also reiterate the importance of joint efforts by all actors, including private creditors, to continue working towards enhancing debt transparency. Bank and IMF support remains critical to enhance debt management and transparency, strengthen countries’ domestic revenue mobilization and spending efficacy, and combat illicit financial flows. Looking forward, we urge the Bank and the IMF to help countries design and implement policies to address the root causes of excessive and unsustainable debt. Many middle-income countries also face severe debt distress, limiting their ability to respond to the pandemic. We ask the Bank and the IMF to identify lessons learned and continue working closely with other organizations and policymakers to address the debt challenges facing middle-income countries, on a case-by-case basis. We welcome the launch of a second voluntary self-assessment of the implementation of the G20 Operational Guidelines for Sustainable Financing. We look forward to further updates on the implementation of the Institute of International Finance Voluntary Principles for Debt Transparency.

The effects of the COVID-19 crisis will be felt for years. Mobility restrictions and lockdowns have triggered job losses, especially for women, youth, and vulnerable groups, and can undermine social inclusion. School closures have caused unprecedented disruption to education, especially for girls, damaging human capital, with long-term economic implications. Inflation and depleted incomes have raised household indebtedness and food insecurity. We urge the WBG to scale up its work to address rising levels of food insecurity and to support countries in achieving SDG2 and nutrition for all. It should address the medium and longer-term challenges of food security and nutrition in a programmatic way and in partnership with other multilaterals, while supporting countries in responding rapidly to already deteriorating food security conditions. Fragility, conflict, and violence (FCV) have worsened in many regions. It is urgent to address drivers of FCV, as well as forced displacement and migration. We look forward to the implementation of the FCV strategy. A sustainable and inclusive recovery requires addressing financial sector vulnerabilities, eliminating tax evasion, and mobilizing vital investments. Priorities for investment include quality health care, nutrition, and education; social safety nets; digital and other innovative technologies; sustainable and quality infrastructure; access to energy, including renewable resources; broader opportunities for women and girls; and finance for SMEs and microenterprises. We urge the WBG to help all client countries revitalize trade, support foreign direct investment, and preserve and create jobs. We note the serious impact of the pandemic in many small states and middle-income countries, where new risks and vulnerabilities are arising; and we urge the WBG and the IMF to strengthen efforts to support these countries, in line with their mandates. We welcome the GRID approach and ask the WBG for its effective implementation through country strategies and operations. The WBG is uniquely positioned to tackle the challenges ahead through its convening power, global reach, and capacity to mobilize finance, technical assistance, and knowledge for both the public and private sectors.

We commend the WBG’s scale-up of climate finance over the past two years, its continuing role as the largest multilateral source of climate investments in developing countries, its emphasis on biodiversity, and its technical and financial support for adaptation, mitigation, and resilience. We also welcome the WBG and IMF’s work to assess the impact of climate change on macroeconomic and financial stability. In addressing immediate infrastructure and economic needs, we request that the WBG continue working with clients to address climate change, land degradation, and biodiversity loss, while ensuring affordable and cleaner energy access. We ask the Bank to ramp up its comprehensive work on biodiversity and work on measuring co-benefits and mainstreaming biodiversity in its operations, as appropriate. We further encourage the WBG and IMF to support a measurable impact in the transition to a low-carbon economy, while considering countries’ energy needs and mix, and providing targeted support for the poorest. These efforts will include phasing out of inefficient energy subsidies and other distortive fiscal policies where feasible. The most impoverished and vulnerable populations, including those in FCV situations and small states, are among those most affected by climate change, damaged ecosystems, and natural disasters. We support the WBG’s ambitious new target to direct 35% of its financing to climate on average, its commitment for at least 50% of Bank climate financing to support adaptation and resilience, and its crucial convening and knowledge-sharing role and support to a just transition, for countries that request such support. We look forward to the WBG’s Climate Change Action Plan for 2021-2025 and recognize its work on disaster risk management, preparedness, and response. We welcome the WBG’s proposal to conduct Country Climate and Development Reports and emphasize that Nationally Determined Contributions (NDCs) should be the primary focus of climate strategies. We commend the WBG’s commitment to align its financial flows with the Paris Agreement, and to continue helping countries reach their climate goals, including through NDCs and National Biodiversity Strategies and Action Plans. We also encourage IFC and MIGA’s efforts to mobilize Paris-aligned private sector investments. We support the WBG’s and the IMF’s important role in preparations for the CBD COP15, UNCCD COP15, and UNFCCC COP26 meetings later this year.

A vibrant private sector will be essential for client countries to recover, create jobs, and embrace economic transformation. We urge the WBG to continue its work to help crowd-in private capital and finance, and to support the private sector. This should build on the IFC 3.0 Strategy to create markets. IFC should continue helping companies create jobs, preserve viable businesses, adapt to the changes brought by COVID, and pursue a green recovery. We ask MIGA to continue addressing the needs for short- and longer-term funding of private investors and lenders.

We support the frontloading of IDA19 resources from FY23 to FY22 to help the poorest countries in their immediate response to the COVID-19 crisis. We also welcome advancing IDA20 by one year. An ambitious and successful IDA replenishment by December 2021, underpinned by a strong policy framework, will support a green, resilient, and inclusive recovery in IDA countries as they address both the immediate and longer-term impacts of the pandemic. We ask the WBG to propose ways to optimize IDA’s balance sheet to make the most of donor contributions and IDA resources, while preserving its AAA rating.

The next meeting of the Development Committee is scheduled for October 15, 2021, in Washington, DC.

Communiqué of the Forty-third Meeting of the IMFC

Chaired by Ms. Magdalena Andersson, Minister for Finance of Sweden

April 8, 2021

The Committee expresses its deep appreciation to Governor Lesetja Kganyago for his leadership as IMFC Chair and welcomes Minister Magdalena Andersson as the new Chair.

We express our sympathies for the loss of human lives caused by the COVID-19 pandemic and the suffering it has entailed. We will continue to work together to end the pandemic everywhere and secure a strong, sustainable, balanced, and inclusive recovery.

The global economy is recovering from the crisis faster than expected last October, thanks to an unprecedented policy response and rapid progress in vaccine development. But the prospects for recovery are highly uncertain and uneven within and across countries due to varying policy space, different economic structures and rigidities, preexisting vulnerabilities, and uneven access to vaccines. Elevated financial vulnerabilities could pose risks, should global financial conditions tighten swiftly. The crisis may cause extended scarring and exacerbate poverty and inequalities, while climate change and other shared challenges are becoming more pressing.

We will calibrate our policies and strengthen cooperation to durably exit the crisis. We emphasize the need for strong international cooperation to accelerate vaccine production and support affordable and equitable distribution to all. To that end, we continue to support the work of the World Health Organization, the ACT Accelerator collaboration, and its COVAX Facility. We will maintain our policy support, tailored to country circumstances, until constraints on economic activity ease meaningfully, continuing to prioritize health spending and assistance for the most vulnerable, while preserving long-term fiscal sustainability. Where appropriate, monetary policy should remain accommodative, in line with central banks’ mandates. We will continue to monitor and, as necessary, tackle financial vulnerabilities and risks to financial stability, including with macroprudential policies. We will continue to monitor and cooperate to reduce excessive global imbalances over time through macroeconomic and structural policies that support sustainable global growth.

Strong fundamentals and sound policies are essential to the stability of the international monetary system. We remain committed that our exchange rates reflect underlying economic fundamentals and note that exchange rate flexibility can facilitate the adjustment of our economies. We will continue to consult closely on foreign exchange market developments. We recognize that excessive volatility or disorderly movements in exchange rates can have adverse implications for economic and financial stability. We will refrain from competitive devaluations and will not target our exchange rates for competitive purposes.

We will also strengthen multilateral cooperation to ensure an inclusive and resilient global economy. In line with the Paris Agreement, we commit strongly to addressing climate change through measures to accelerate the transitions to greener societies and job-rich economies, while protecting those adversely affected. These comprise a range of fiscal, market, and regulatory actions, mechanisms, and policy mixes, taking into account country-specific factors. We will continue to collaborate to unlock the potential of the digital economy, and accelerate efforts toward a modern and globally fair international tax system. We reaffirm our commitment to strong governance, including by tackling corruption. We agree on the need to promote more open, stable, fair, and transparent trade policies and to modernize the rules-based trading system under the World Trade Organization, which are key to boosting global growth. We are taking comprehensive action to help vulnerable countries meet their financing needs. We will work together to continue strengthening debt transparency practices by both debtors and creditors, public and private, and supporting countries’ efforts to maintain debt sustainability. Where appropriate, we will facilitate swift debt treatment together with broad participation by official and private creditors in line with the comparability of treatment principle.

We welcome the Managing Director’s Global Policy Agenda.

We welcome the IMF’s efforts to help members toward a sustained recovery from the crisis. We call on the IMF to make a comprehensive proposal on a new Special Drawing Rights (SDR) general allocation of US$650 billion to help meet the long-term global need to supplement reserves, while enhancing transparency and accountability in the reporting and the use of SDRs.

We welcome the IMF’s support to help members transition to upper-credit-tranche-quality programs for countries that move out of the emergency phase of the crisis. We call on the IMF to explore how to further support vulnerable low-income and middle-income countries in line with its mandate. We call on the IMF to work with its members to continue exploring ways for voluntary post-allocation channeling of SDRs to support members’ recovery efforts. We support the IMF to explore reforms to its concessional financing instruments for low-income countries and to increase the lending capacity of the Poverty Reduction and Growth Trust, and to secure sufficient contributions for a final tranche of debt service relief from the Catastrophe Containment and Relief Trust, including from new participants for both trusts. We support the IMF’s enhanced assistance to help address particular challenges faced by fragile and conflict-affected states, small states, and countries hosting refugees. We encourage members to contribute to Sudan’s financing package for the clearance of arrears to the IMF and debt relief under the Enhanced Heavily Indebted Poor Countries Initiative. We welcome the IMF’s work on advancing the debt agenda jointly with the World Bank, including by continuing to support the effective implementation of the G20 Debt Service Suspension Initiative and Common Framework, which are also agreed by the Paris Club, and by reviewing key policies and rolling out enhanced tools to support efficient implementation of sovereign debt restructuring.

We highlight the critical role of surveillance in providing cutting-edge policy advice and macro-financial analysis tailored to country circumstances, supported by targeted capacity development. We look forward to the review of the IMF’s Institutional View on capital flows, informed by, among others, the Integrated Policy Framework. The IMF has an important role in responding to members’ diverse needs for guidance on the macroeconomic and financial implications of climate change issues. We, therefore, support the IMF in stepping up work to help its members identify and manage the macro-critical implications of climate change, digitalization, inequality, and fragility, in close collaboration with partners, and to further integrate these issues into its surveillance, lending, and capacity development in line with its mandate. We will explore the appropriate budget envelope for ensuring that the IMF has the staff and skills required to carry out its mandate. We also support ongoing modernization projects and call for further progress on diversity.

We reaffirm our commitment to a strong, quota-based, and adequately resourced IMF at the center of the global financial safety net. We welcome the effectiveness of the doubling of the New Arrangements to Borrow and of the new round of bilateral borrowing agreements. We remain committed to revisiting the adequacy of quotas and will continue the process of IMF governance reform under the 16th General Review of Quotas, including a new quota formula as a guide, by December 15, 2023. We welcome the start of this work and look forward to the first progress report by the time of the Annual Meetings.

Our next meeting is expected to be held on October 14, 2021.

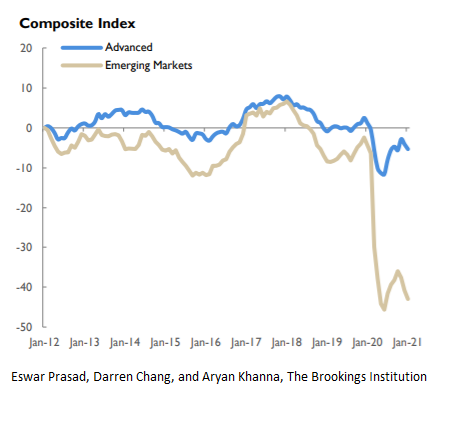

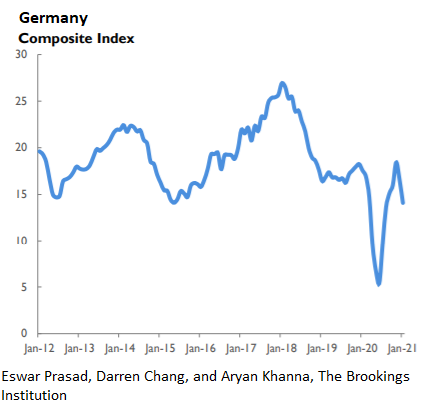

While the US, China, and other leading economies are on their way to a robust recovery, many others are struggling to return to pre-pandemic GDP levels. In most regions, including Europe and Latin America, the 2020 recession will most likely leave long-lasting scars on both GDP and employment.

The chances for a swift, uniform rebound from the COVID-19 crisis have dimmed, and the world economy now faces sharply divergent growth prospects. Although the latest update of the Brookings-Financial Times Tracking Indexes for the Global Economic Recovery (TIGER) offers some grounds for optimism, it also raises renewed concerns. Vaccination euphoria has been tempered by slow vaccine rollouts in most countries, while fresh waves of COVID-19 infections are threatening many economies’ growth trajectories.

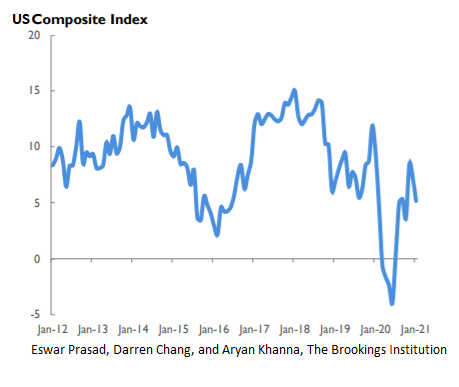

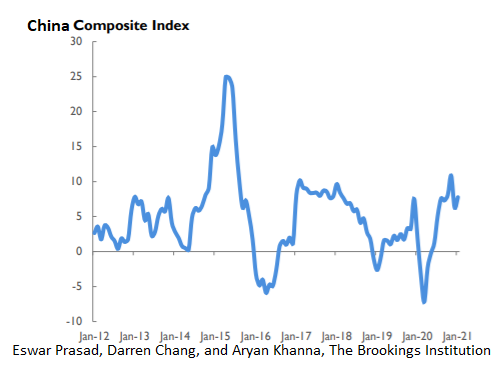

The US and China are shaping up to be the main drivers of global growth in 2021. Household consumption and business investment have surged in both economies, along with measures of private-sector confidence. Industrial production has rebounded in most countries, firming up commodity prices and international trade. Nonetheless, the US, China, India, Indonesia, and South Korea will probably be the only major economies to exceed pre-pandemic GDP levels by the end of this year. In most other regions, the 2020 recession will most likely leave longer-lasting scars on both GDP and employment.

The US economy is poised for a breakout year, as massive fiscal stimulus, loose monetary policies, and pent-up demand translate into rapid GDP growth. Renewed consumer and business confidence has led to generally strong consumption and investment growth, and financial markets have continued to perform well. Even labor market performance has been more encouraging, with 916,000 new jobs added in March, more than double the total for February and the most since last August.

The task for monetary policymakers this year will be to separate phantom inflation (the imminent bounce-back after 2020) from underlying wage and price pressures. The rise in government bond yields – which reflects a combination of better growth prospects, inflation risk, and debt concerns – reflects the challenges that policymakers will face as they try to decipher and manage market expectations. Ideally, any additional stimulus measures will aim to boost aggregate demand and improve long-term productivity simultaneously.